The GENIUS Act, which stands for “Guiding and Establishing National Innovation for U.S. Stablecoins,” is a federal rulebook that outlines how stablecoin issuers must operate in order to stay compliant and secure. Passed in the Senate on June 19th by a vote of 68-30, the bill still requires approval from the House of Representatives.

There is significant optimism that the bill will pass in the House, especially since a similar bill, the Stablecoin Act, had previously received approval. Industry leaders, such as Tether’s CEO, have expressed excitement, seeing benefits for established players. Additionally, Circle’s stock price has risen following the bill’s passage, suggesting positive market sentiment.

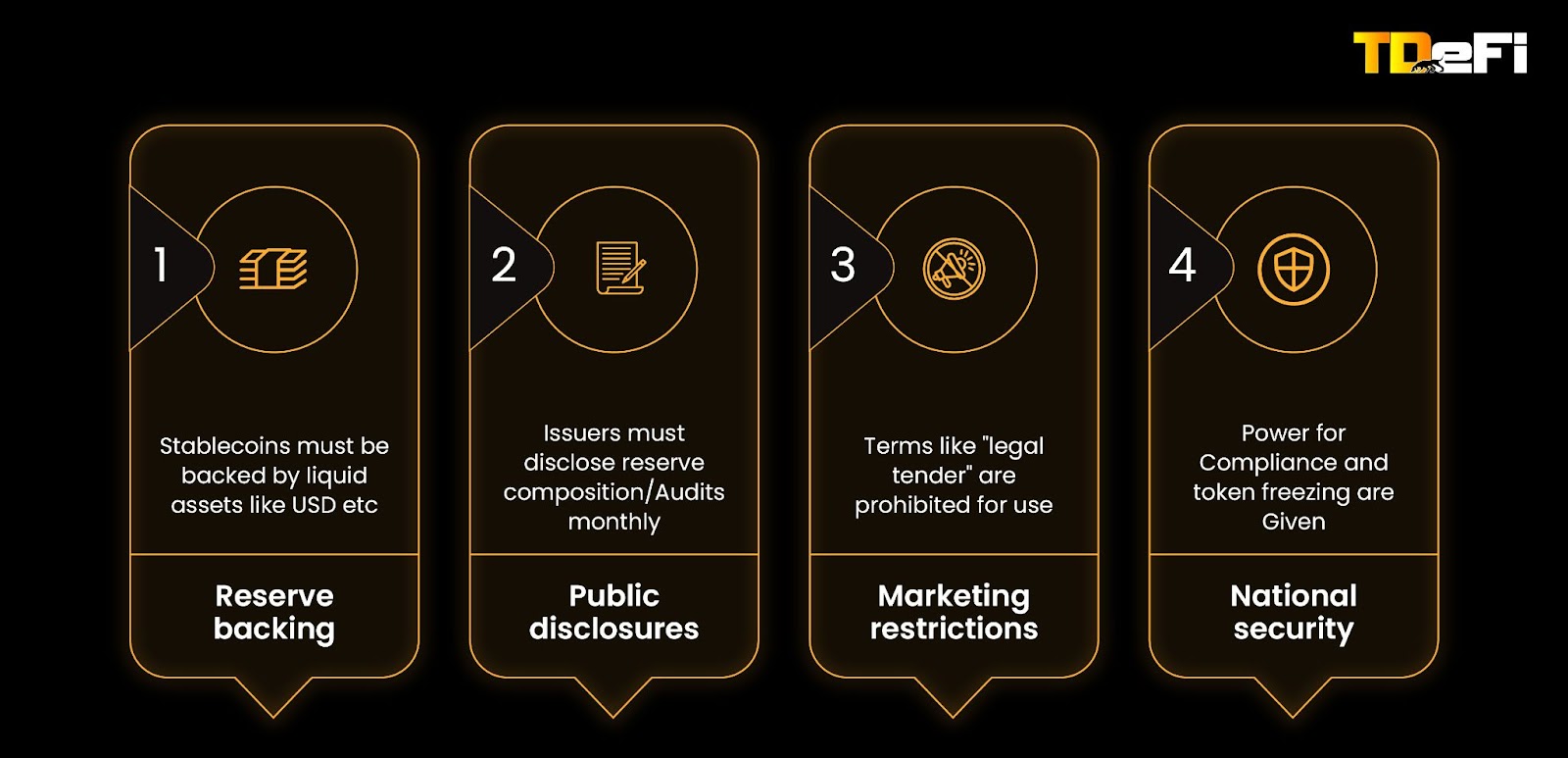

The direct impact of the bill are:

- Will allow payments in stablecoins.

- The Stablecoins issued must be backed 1:1 by any liquid assets.

- This will be the first major crypto regulation.

Public Reactions:

While many in the crypto industry and some lawmakers view the GENIUS Act as a milestone that could boost adoption and trust by providing regulatory clarity, others are raising concerns. Some worry about over-regulation, insufficient consumer protections, and the potential for market concentration, with large entities dominating the space. There is also a growing view that the act could hinder innovation.

Professors like Ravi Sarathy have voiced skepticism, saying, “I don’t see anything of the sort in the GENIUS Act,” with others adding that it could be “worse than no bill at all.” Online discussions, particularly on Reddit, have been critical, with users calling it “garbage legislation” and likening it to a “CBDC wrapped in stablecoin lingo.” There are also fears regarding the potential impact on yields and innovation within the stablecoin sector.

Concerns About the GENIUS Act:

- The GENIUS Act forces issuers to hold 100 % cash-and-T-bill reserves, yet it never extends deposit-insurance coverage (the kind bank customers enjoy up to $250 k). If an issuer collapses or a hacker drains our wallet there’s no federal insurer swooping in with a guaranteed payout

- Wild Cat Banking: A New Yorker analysis warns that letting dozens of private tokens compete without an explicit lender of last resort could recreate 19th-century “wild-cat banking,” where panics spread through notes no one trusted.

- Also some believe that new compliance costs could thin out smaller players, like the monthly audits

- The Issuers now can’t gamble customer funds on risky stuff; most reserves must sit in cash or T-bills, providing a liquidation problem for the institutions

Conclusion

While the GENIUS Act finally brings regulatory clarity to the stablecoin space, its requirement that issuers hold 100 % of user funds in cash and ultra-safe T-bills effectively strips away their ability to generate meaningful returns—and in turn denies users any real yield. At today’s T-bill rates (hovering around 5 % annually), once you subtract the costs of monthly audits, compliance overhead, and operational expenses, net returns to issuers—and ultimately to users.

This is a fundamental shift: stablecoins have long been prized not just for dollar-pegged stability, but for their integration into DeFi protocols that deliver double-digit yields. By forcing capital to sit idle in low-return instruments, the Act turns stablecoins into digital checking accounts that pay worse rates than traditional banks—and without FDIC insurance to boot in case of hacks.

“The stablecoin bill creates a transmission channel from the extremely volatile crypto ecosystem to the traditional financial sector, and that’s incredibly dangerous,” Frayer (During the Biden Administration, Frayer served as an adviser on crypto issues to Gensler at the S.E.C. Several times in recent years) said.

Until regulators allow a more balanced reserve framework—one that preserves safety without gutting yield—stablecoins will struggle to compete as a viable financial plumbing in crypto. In its current form, the GENIUS Act risks stifling innovation, driving users back to legacy banks or unregulated markets in search of returns, and undermining the very adoption it aims to foster.